Choppy Waters, Hidden Currents

Thoughts on the Market

Nvidia didn’t break out, and Financials didn’t break down.

That pretty much sums up last week’s trading action and tells us one thing: we’re still stuck! There’s little appetite to chase strong news, but at the same time investors continue to treat the market’s weak spots as isolated issues.

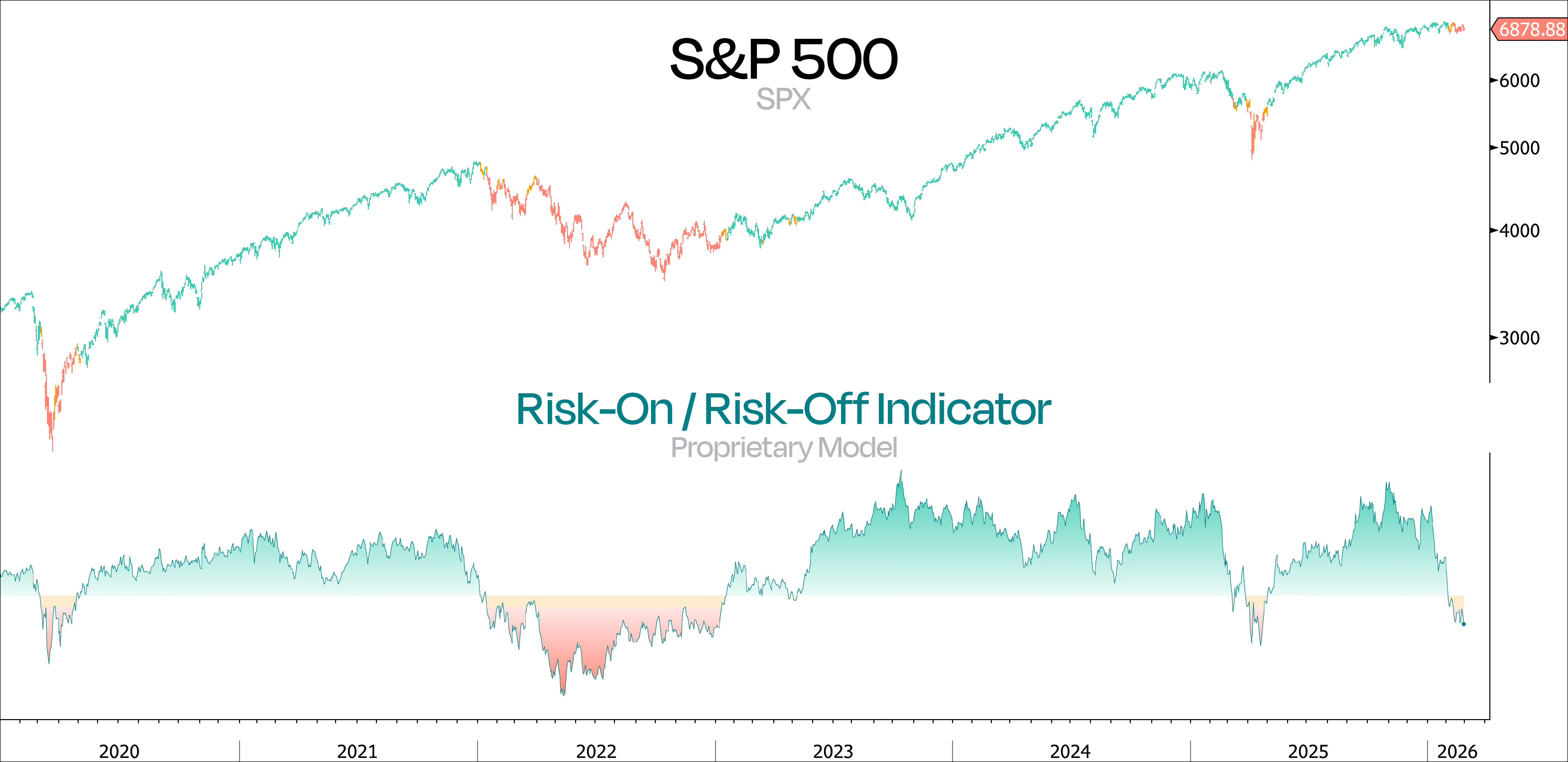

However, a quick look at the VIX Index, which is still above 20 — a level historically favored by bears — shows that overall risk appetite is still muted. And that’s exactly what our Proprietary Risk Appetite Model has been signaling for almost a month now.

As long as the S&P 500 keeps moving sideways, we don’t expect much to change in the model. But when this range finally breaks, the direction of that move will certainly matter.

Going forward, we’ll keep a close eye on Financials and Technology as discussed last week, since they’re still the most likely sectors to drag the index lower. That said, as we emphasized before, it will be just as important to watch for early signs that positive momentum might be coming back.

On that front, one bright spot from last week’s choppy price action was the ARKK ETF further invalidating the potential Head & Shoulders top. The group of high-flying innovation names finished the week up 2%, continues to hold above the neckline, and is still trading above the anchored VWAP from the April lows.

In short, selling pressure hasn’t been strong enough to break it down, which tells us there’s still underlying strength in this market.

Moving on, we’re two months into the year, and our small-cap trade has been one of the clear outperformers so far.

The Russell 2000 has beaten the S&P 500 by nearly six percentage points year-to-date and is up almost 13% since we first suggested rotating out of the heavily concentrated indexes back in late August.

To be clear, the move into small-caps wasn’t just about leaning into that theme. It was also about stepping a bit further out on the risk curve — and despite everything that’s happened since, that decision has held up well.

As the next chart shows, the Russell 2000 is still pushing up against its multi-year downtrend relative to the S&P 500.

As we’ve said over and over, small-caps really need two things to keep working:

Financial conditions need to be easing, and

Economic activity needs to be picking up.

Lately, rates have been doing their part. They’ve been falling, which helps loosen financial conditions. On the surface, that’s exactly what you’d want if you’re constructive on small-caps.

The issue, though, isn’t the move itself — it’s the reason behind it.

The narrative has shifted pretty quickly from “the economy is strong” to something closer to “we’re all about to become unemployed.” So for the first time, those AI fears seem to be creeping into the rates market.

The roughly 20-basis-point drop in the US 10-year yield this year really stands out, especially considering that economic data over the past two months has actually been reaccelerating. A quick look at the Citigroup Economic Surprise Index backs that up — activity has been coming in stronger than expected, just as we’ve been highlighting for months.

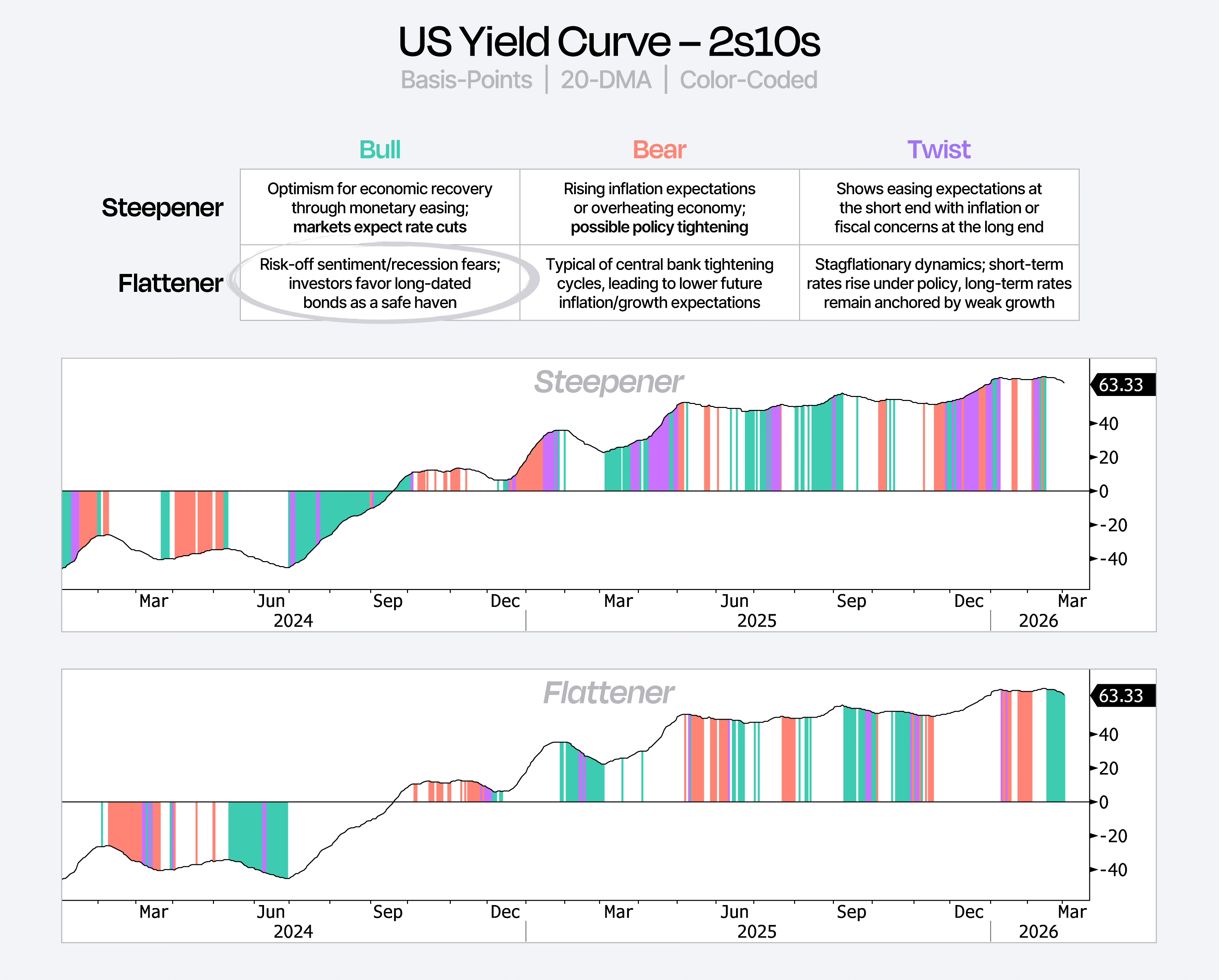

So, what do bonds know?

If you look at the US 2s10s yield curve — the spread between the 2-year and 10-year Treasury yields — we can see that after moving mostly sideways for about nine months, it started to roll over in February. In market terms, the curve began to flatten.

Because yields have been falling across the board, the flattening is happening because long-term yields are dropping faster than short-term yields. That’s what’s known as a bull flattener.

Our table below shows that a bull flattener almost always means that the bond market is pricing in weaker long-term growth and rising risk aversion.

In plain English, it’s a flight to safety.

Like we’ve said, this is helping loosen financial conditions even more — and our next chart below makes it pretty clear.

Keep reading with a 7-day free trial

Subscribe to Duality Research to keep reading this post and get 7 days of free access to the full post archives.