Expensive Narrative, Cheap Reality

Thoughts on the Market

We’ve been firmly bullish for well over a month now.

Five weeks ago, in our note titled The Quiet Signals: Tracking Early Signs of Stability, we pointed out the historically powerful setup developing in Semis after that massive momentum thrust off the lows. At the same time, we highlighted something the market wasn’t fully appreciating yet: despite higher oil prices, the Dollar Index, VIX, and credit spreads all failed to make new highs. That mattered.

Four weeks ago, in It Feels Early, It Feels Uncomfortable — And That’s Usually the Point, we recommended overweighting Technology, as the relative setup vs the S&P 500 suggested leadership was about to rotate back in its favor. Since then, the Tech ETF (XLK) has ripped 23% in just four weeks!

Three weeks ago, in 8000 in 10 Weeks — And Nobody’s Ready, we doubled down on our bullish view and laid out the case for the S&P 500 pushing toward 8000 by the end of June, driven largely by concentrated gains in big Tech.

Throughout all of this, our message was simple: avoid static thinking and focus on where things are headed, rather than where they stand today. Because as long as the rate-of-change continues to move in our favor, remaining constructive and leaning into that trend is likely to pay off.

It has paid off, and catching the leaders in this historic rally has been extremely profitable.

At the same time, we can’t ignore how quickly sentiment seems to have shifted compared to the rebound after last year’s tariff scare. The crowd has embraced this rally much faster this time around, and that’s definitely something we’re paying close attention to here — especially with NVIDIA’s earnings still about 10 days away.

But zooming out, the bigger picture hasn’t changed much in our view. The path toward a meaningfully higher S&P 500 into next month is still very much alive.

This is still a bull market, so let’s act accordingly.

Since we’ll be taking next week off — meaning there won’t be a Thoughts on the Market note next Monday — we wanted to use today’s note to step back a bit and touch on a few bigger-picture topics: the labor market, our main takeaway from this still ongoing earnings season, and what looks to be the end of the current Breadth Thrust Regime.

So with that, let’s jump straight into the jobs data from last week.

For a while now, we’ve been making the case that the labor market isn’t just stabilizing — it’s actually re-accelerating. Last week’s Continuing Claims print added more evidence to that view. Since Continuing Claims are basically the running scorecard between hiring vs firing, the fact they just fell to their lowest level in more than two years tells you that unemployed workers are increasingly finding jobs again at a faster pace. At the same time, Initial Jobless Claims continue to hover near some of the lowest levels of the past 50+ years. In other words, this still remains a very low-firing environment.

Given all that, it wasn’t especially surprising to see April’s Nonfarm Payrolls report come in strong again. The weekly claims data had already been telling us that story for weeks — the payrolls number simply confirmed it.

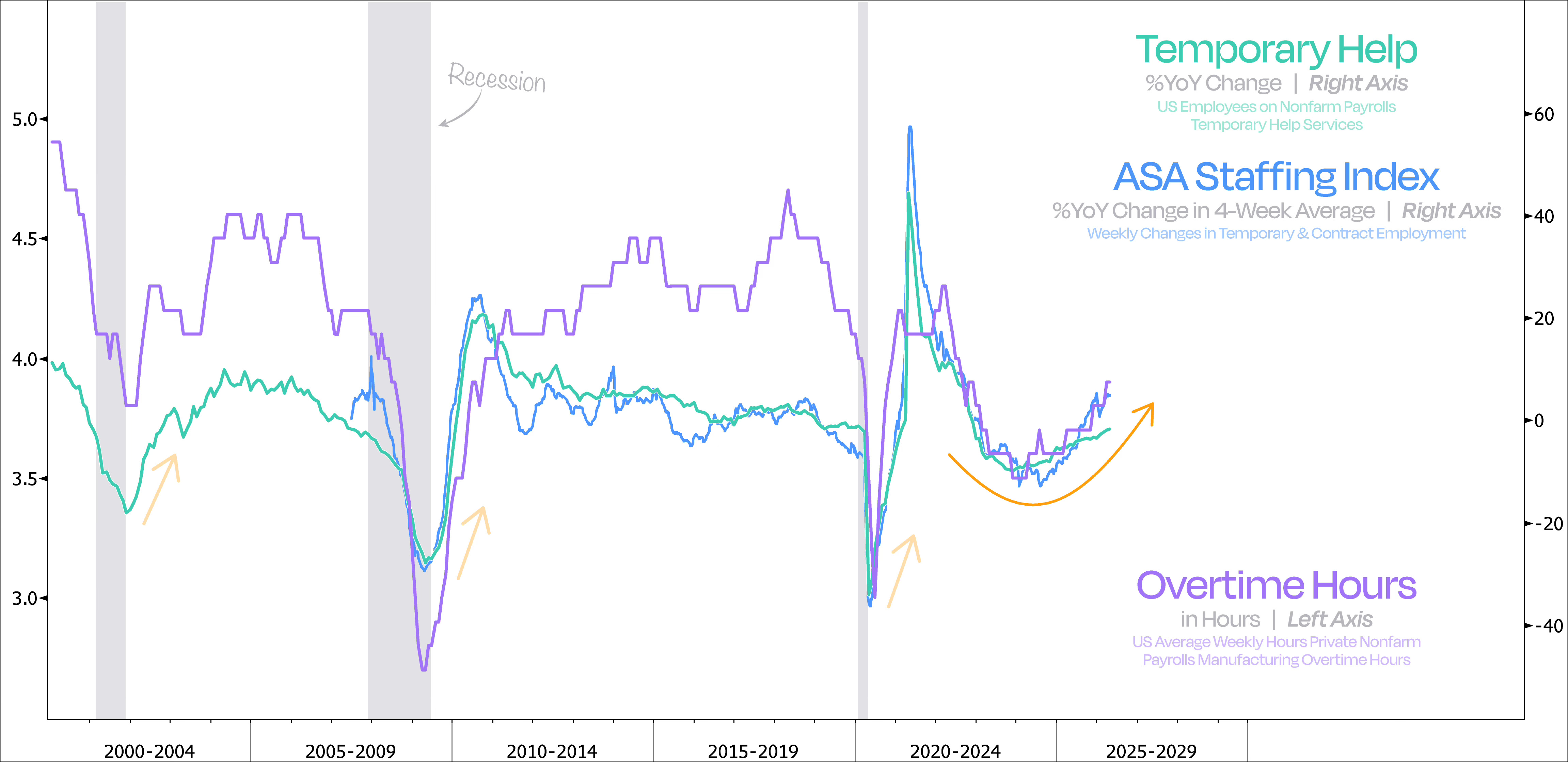

But as always, the real edge comes from looking at the stuff that tends to lead the labor market. For us, that means watching things like Overtime Hours, Temporary Help Services, as well as the ASA Staffing Index, which tracks weekly changes in temporary and contract work. And right now, all of those indicators are still moving in the right direction. As the chart below shows, all three remain in an improving trend, suggesting the recent re-acceleration we’ve been seeing in the ISM still has more room to run.

Historically, these are classic early-cycle signs: businesses see more activity, so they add hours and temps before committing to costly full-time hires.

What’s especially encouraging here is just how broad these improvements have become. More than 50% of roughly 250 sub-industries are now adding jobs — the highest reading we’ve seen in over two years on a rolling 3-month basis.

Keep reading with a 7-day free trial

Subscribe to Duality Research to keep reading this post and get 7 days of free access to the full post archives.