Priced for a Different Regime

Thoughts on the Market

By now, you’ve probably read a dozen FOMC takes — what it means, what it really means, the implications, the second-order implications... yada yada yada.

What we’re noticing once again is that the old habit of hanging on every word is alive and well — even with a new Fed chair. It honestly reminds us of a 16-year-old getting a text from their crush and overanalyzing every single word, only to arrive at an interpretation that has almost nothing to do with what was actually meant.

Yes, Warsh didn’t push back against the hawkish repricing like we’d expected. But at the same time, it’s equally important to acknowledge that he didn’t embrace those hawkish expectations either.

Looking back at last week’s meeting, we walked away with two key takeaways.

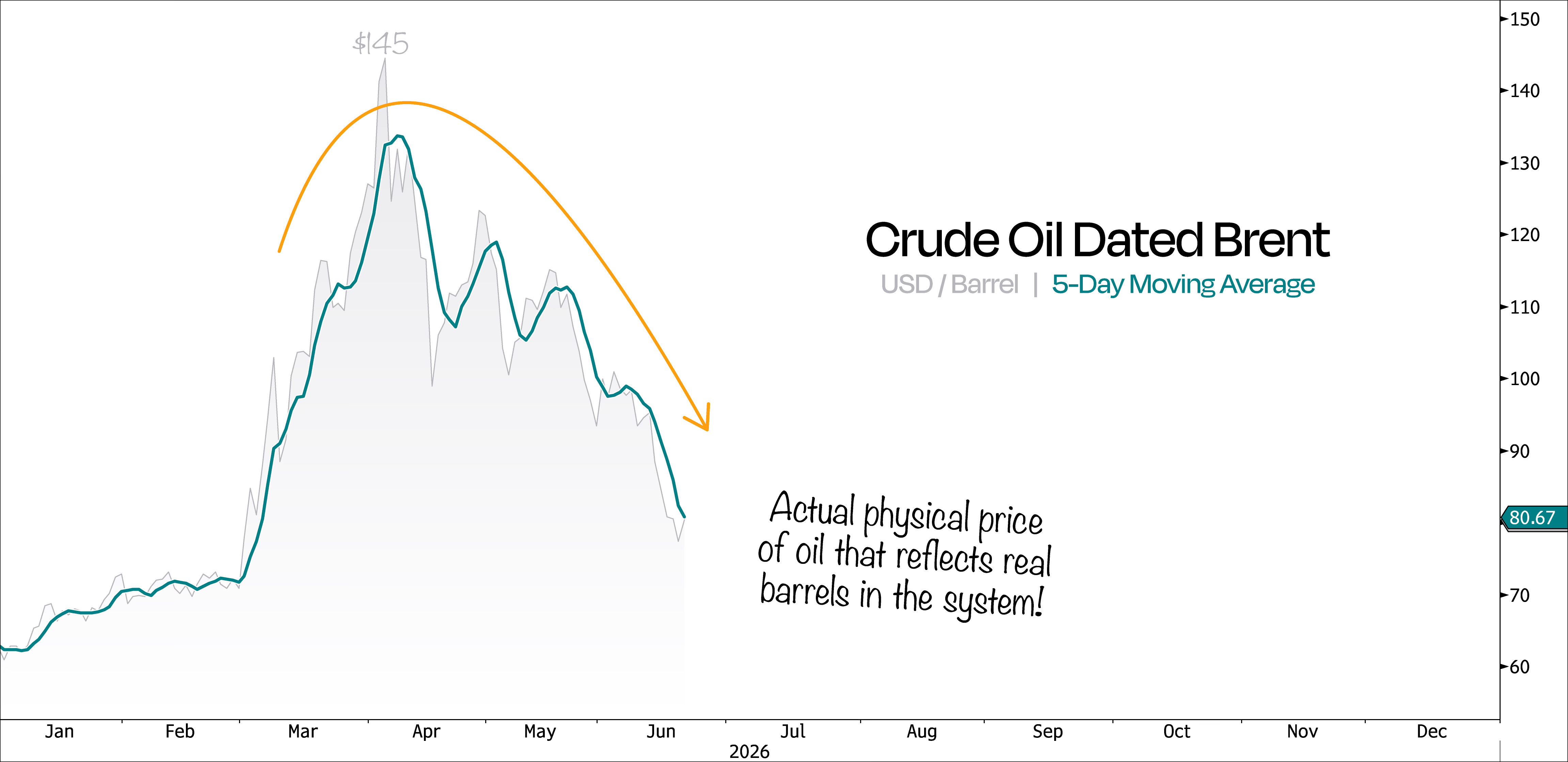

First, Warsh’s priority right now is delivering on price stability. By itself, that’s neither hawkish nor dovish in our view — it all depends on the context. And today’s context is actually pretty straightforward. If higher oil prices were the main catalyst behind the market’s hawkish repricing, then lower oil prices should unwind those expectations again. In other words, if the inflation impulse fades on its own, the Fed doesn’t need to hike to achieve price stability.

This brings us to our second takeaway from last week’s meeting.

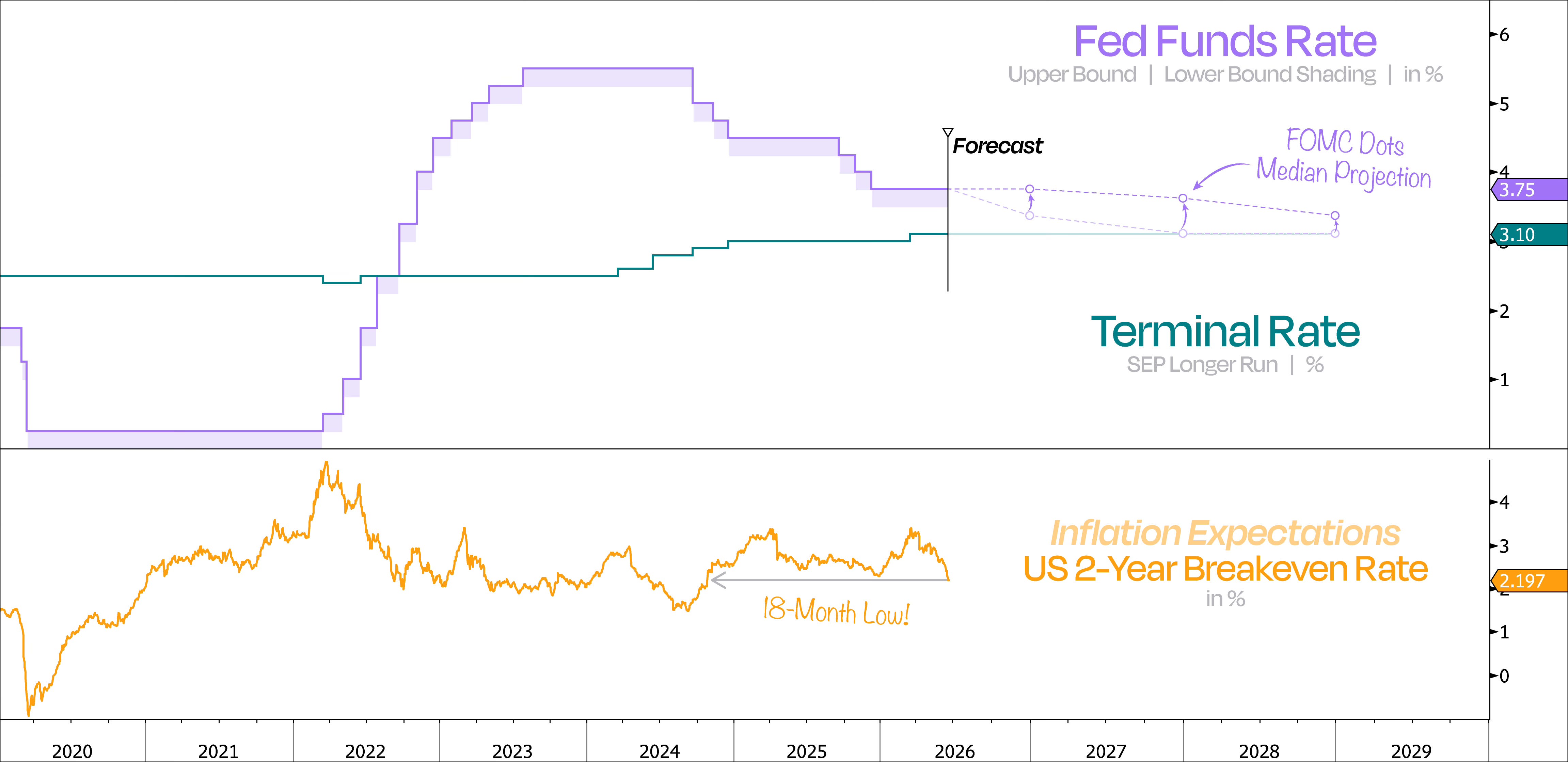

The updated Summary of Economic Projections (SEP) showed fewer rate cuts going forward. And honestly, we don’t blame them. More uncertainty naturally means less conviction in any particular direction.

What many seem to be overlooking, though, is that we didn’t see rate hikes getting penciled in either. The median dot for December 2026 edged up to 3.75%, while the current target range remained unchanged at 3.50–3.75%.

Our next chart shows the Fed’s expected policy path based on the median dot plot. And what it continues to tell us is fairly straightforward: the Fed is willing to hold rates at current levels for a bit longer than it expected a few months ago, but it still ultimately sees the next meaningful move as lower — not higher.

In other words, the message wasn’t “higher for longer forever.” It was “higher for a little longer, then lower.”

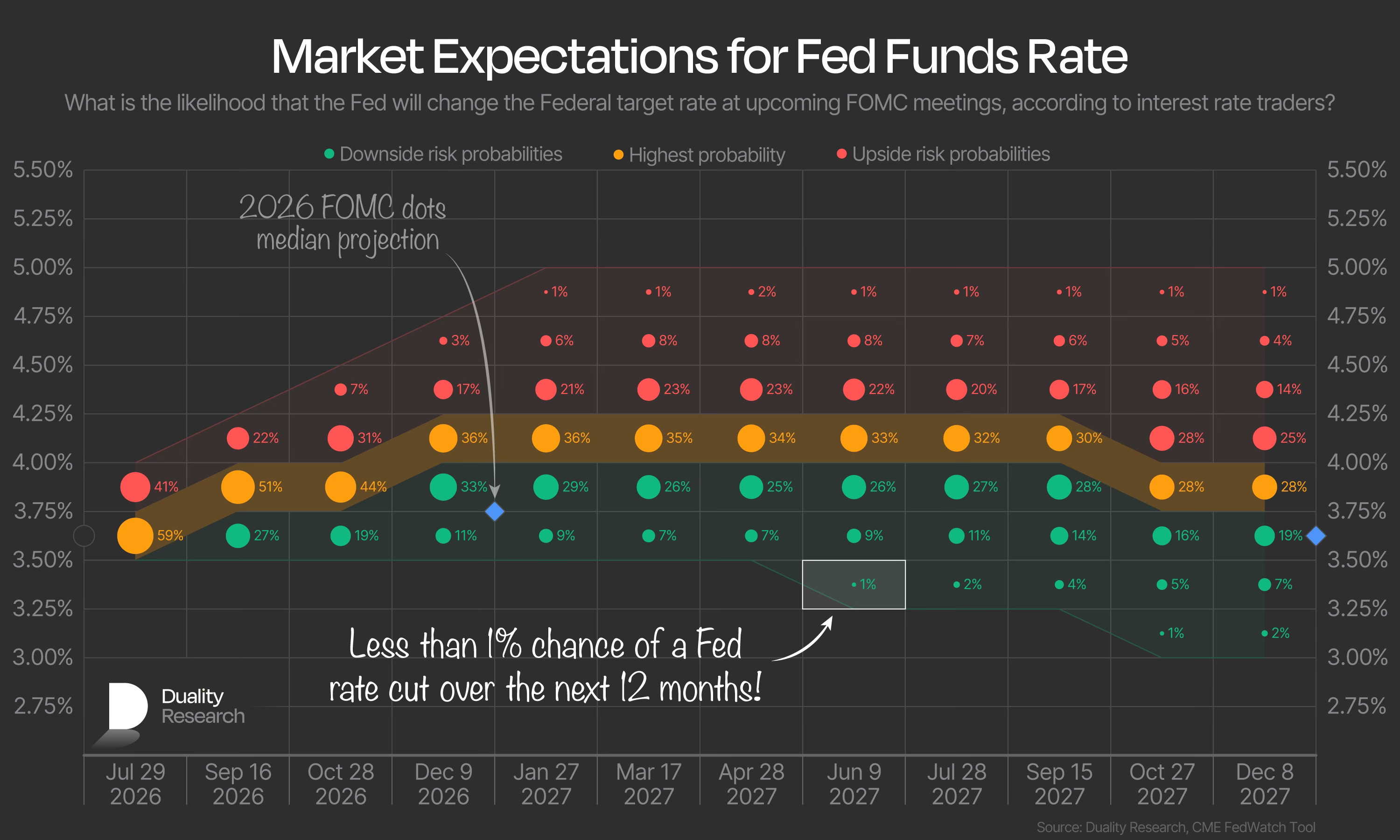

So, if anything, our next chart — which shows the Fed Funds path implied by the futures market — should look exactly the opposite. Instead, we’re still looking at peak hawkishness with the market still pricing in less than a 1% chance of a Fed rate cut over the next 12 months.

At this point, we can’t help but be reminded of the old saying, when everyone ends up on the same side of the boat, it doesn’t take much to tip it.

And let’s not forget, the market’s job is to surprise the largest number of people, not the smallest.

So no, this Fed is not going to hike rates once over the remaining six months of this year, only to cut next year. Warsh is focused on price stability, but he also knows that the recent collapse in oil prices is already undoing part of the inflationary pressure we saw earlier.

Now, while that’s our view, we can’t ignore that the market reaction has looked undeniably hawkish, as reflected in the rise in US 2-year yields. The way we were taught to think about this is simple: you play the hand you’re dealt, not the hand you wish you had.

Keep reading with a 7-day free trial

Subscribe to Duality Research to keep reading this post and get 7 days of free access to the full post archives.