Same Target, Different Journey

Thoughts on the Market

No matter how you slice it, the biggest risk to this bull market is a Fed opening the door to rate hikes. That was our main takeaway from last week’s note, where we explored what could ultimately bring this bull run to an end despite the economy remaining in a supportive sweet spot. After all, monetary tightening has often been the catalyst that ends the cycle. And with the economy showing signs of re-acceleration, investors may not take long to question whether it can withstand higher rates without that momentum being derailed.

Having said that, the focus now shifts to Wednesday’s FOMC meeting, where Kevin Warsh will hold his first press conference. While it should be fairly clear that the Fed will keep rates on hold, this meeting is less about the decision itself and more about whether Warsh pushes back against the significant hawkish repricing that has taken place in Fed Funds futures.

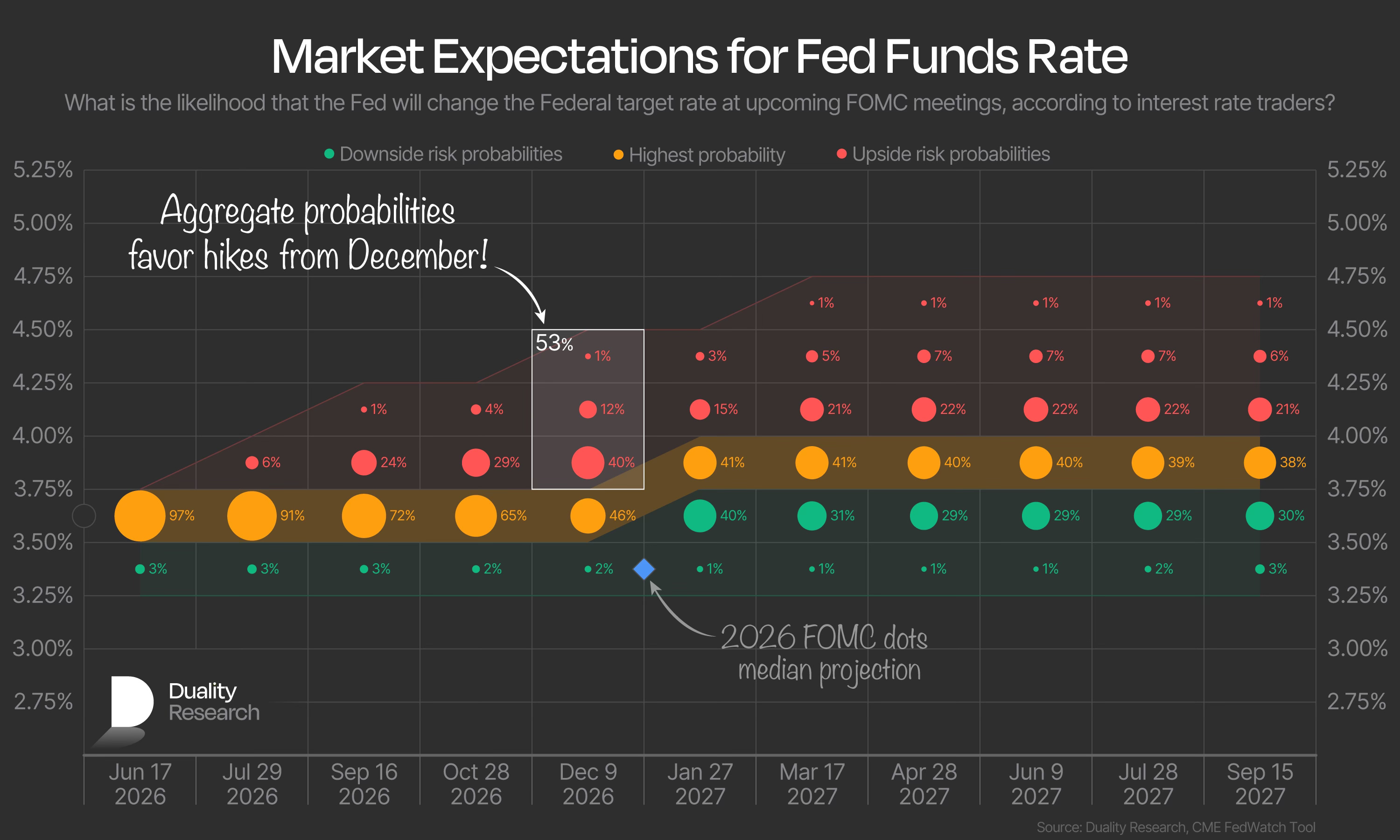

If you look at our first chart for today, you can see the clear upward bias in the rate path that markets have priced in. From December onward, hikes become the base case, and looking further ahead, April next year is the first month where the probability of two or more hikes reach 30%.

Indeed, some investors will see last week’s ECB rate hike — the first by a major central bank in response to the recent energy shock — as adding pressure on the Fed to follow suit. But we think the bar for the Fed to do the same is considerably higher. The key difference is that the ECB started from a much more neutral policy stance, while the Fed is still holding rates at clearly restrictive levels.

And while last week’s inflation report came in elevated again, our main takeaway was that the spillover from higher energy prices into broader inflation remains relatively muted. As long as oil prices continue trending lower — even if they remain elevated in absolute terms — we’re increasingly comfortable saying that this inflation shock is likely behind us. AAA’s national average gas prices are a good example. After surging 36% in March and another 8% in April, prices fell 1.6% in May and are already down more than 6% so far in June.

For us, the takeaway is that while risks remain, the underlying inflation backdrop doesn’t appear to be deteriorating. If anything, it’s moving in the opposite direction. The obvious bear case is that businesses have so far absorbed higher energy costs and simply haven’t passed them on to consumers yet. Our counterargument is straightforward: if they haven’t done so by now, they probably won’t so as long as energy prices continue moving in their favor.

Taken together, the latest inflation data and what we’re seeing in real-time commodity markets should help ease some of the market’s worst fears that Kevin Warsh is about to turn aggressively hawkish.

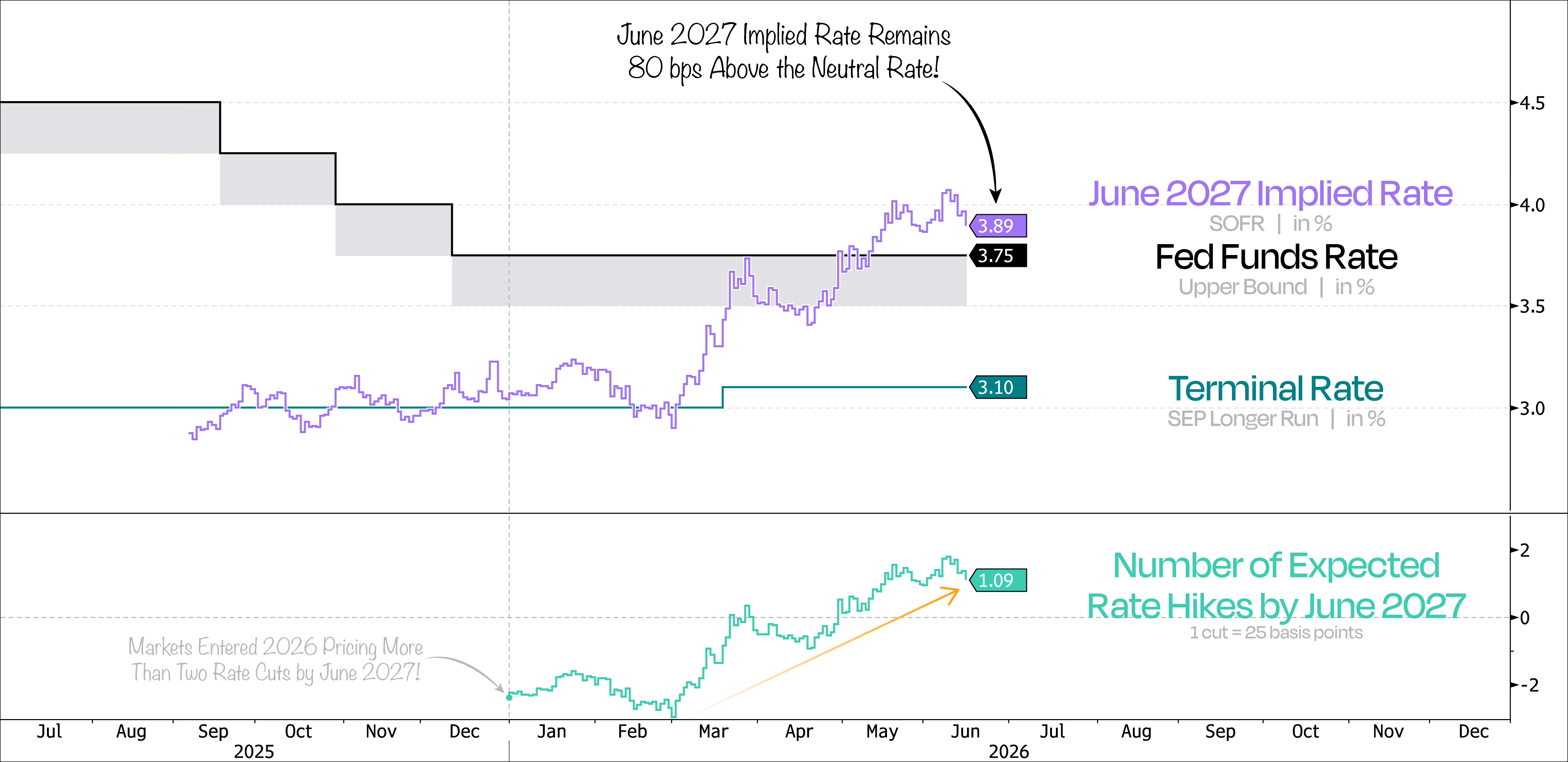

That brings us to our next chart. We came into the year expecting at least two rate cuts over the following 18 months, bringing Fed Funds futures closer to what markets consider the neutral rate. Fast forward six months, and that view has completely flipped. Markets are now pricing in more than one rate hike through June next year, leaving rate expectations roughly 80 basis points above neutral.

In our view, this is another example of the pendulum swinging too far in one direction — a repricing that has clearly started weighing on risk assets. We expect Warsh to push back against that narrative, leading markets to dial back some of their hawkish pricing and, in turn, providing a tailwind for risk assets.

That said, even if peak hawkishness ultimately turns into a tailwind for risk assets, the momentum unwind we’ve seen over the past few trading sessions has likely changed this market for the weeks/months ahead.

Our broader view hasn’t changed — but our roadmap for getting there has. So let’s take a look at what that means for the coming weeks.

Keep reading with a 7-day free trial

Subscribe to Duality Research to keep reading this post and get 7 days of free access to the full post archives.