Second-Half Setup: Peak Everything, Not Peak Equity

Thoughts on the Market

As we head into the second half of what has already been an eventful year, it’s a good time to zoom out and put the bigger picture back into focus. Markets have moved fast, the narrative has shifted more than once, so it’s time to share some context around what we think is reasonable to expect for the remainder of the year.

When we kicked off 2026, we wrote that "anything from geopolitical surprises to shakeups at the Fed could throw curveballs our way." Looking back, that feels almost understated. We’ve had plenty of both. But if there’s one thing markets keep reminding us, it’s that every challenge tends to come with an opportunity.

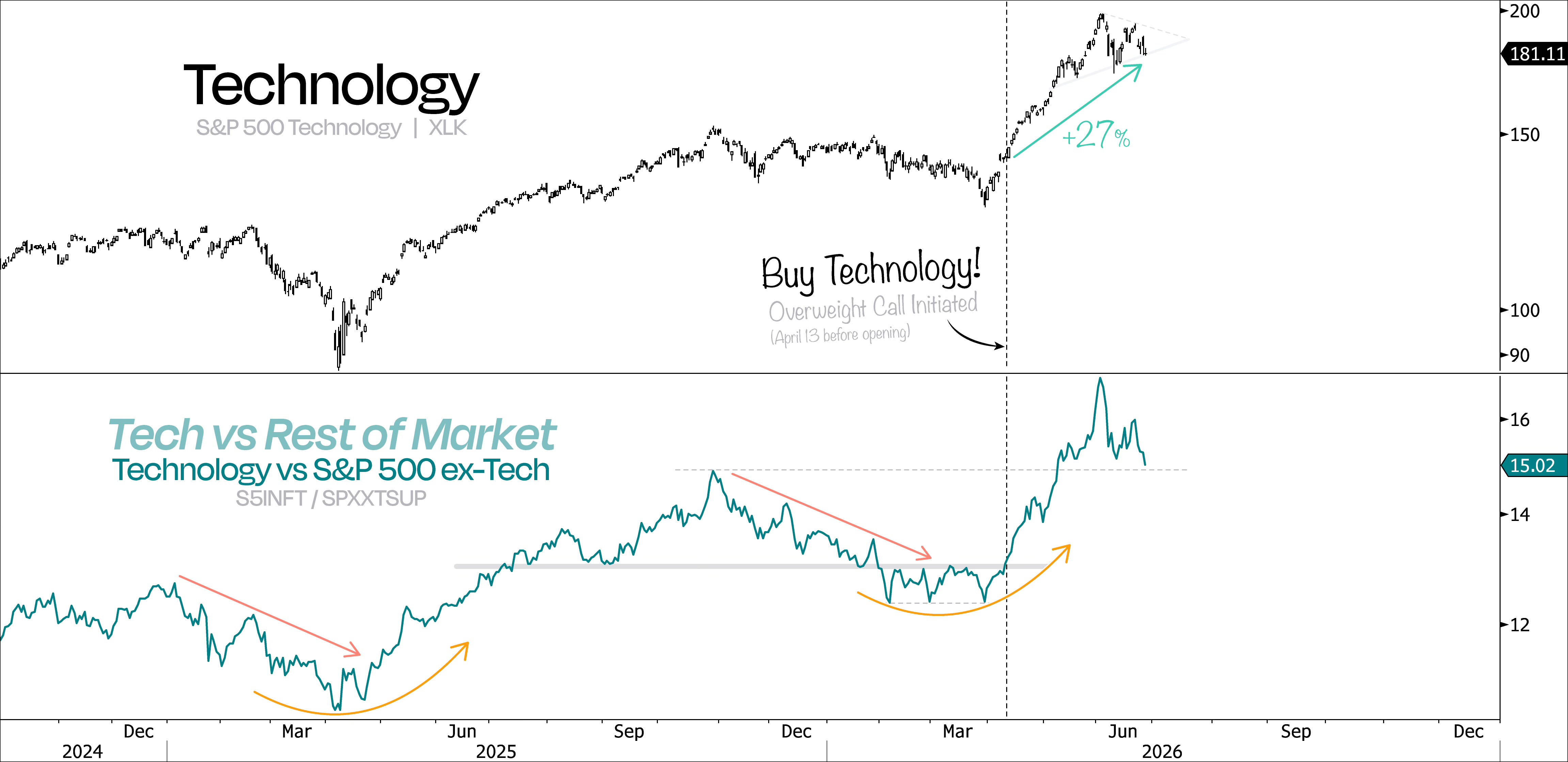

During the first half of the year, that meant fading peak geopolitical uncertainty and peak inflation fears. We didn’t waste much time putting that view to work, expressing it through an overweight in Tech — which ended up working out very well.

Now, as we move into the second half of 2026, the backdrop is changing again. This time, we’re dealing with peak growth and peak hawkishness. We’ve already made it clear that we’re willing to fade the latter. The bigger question now is: what’s the best trade to express that view?

Before we get there, though, let’s first take a step back and look at the bigger picture!

Like we’ve been saying for some time now, the backdrop for the US economy remains broadly supportive. That means a recession isn’t our base case for the remainder of 2026 — or as we head into next year. And that’s an important starting point. If the economy keeps holding up, there’s a good chance earnings estimates will too. Sure, analysts will tweak the numbers along the way, but the broader direction should continue to be higher.

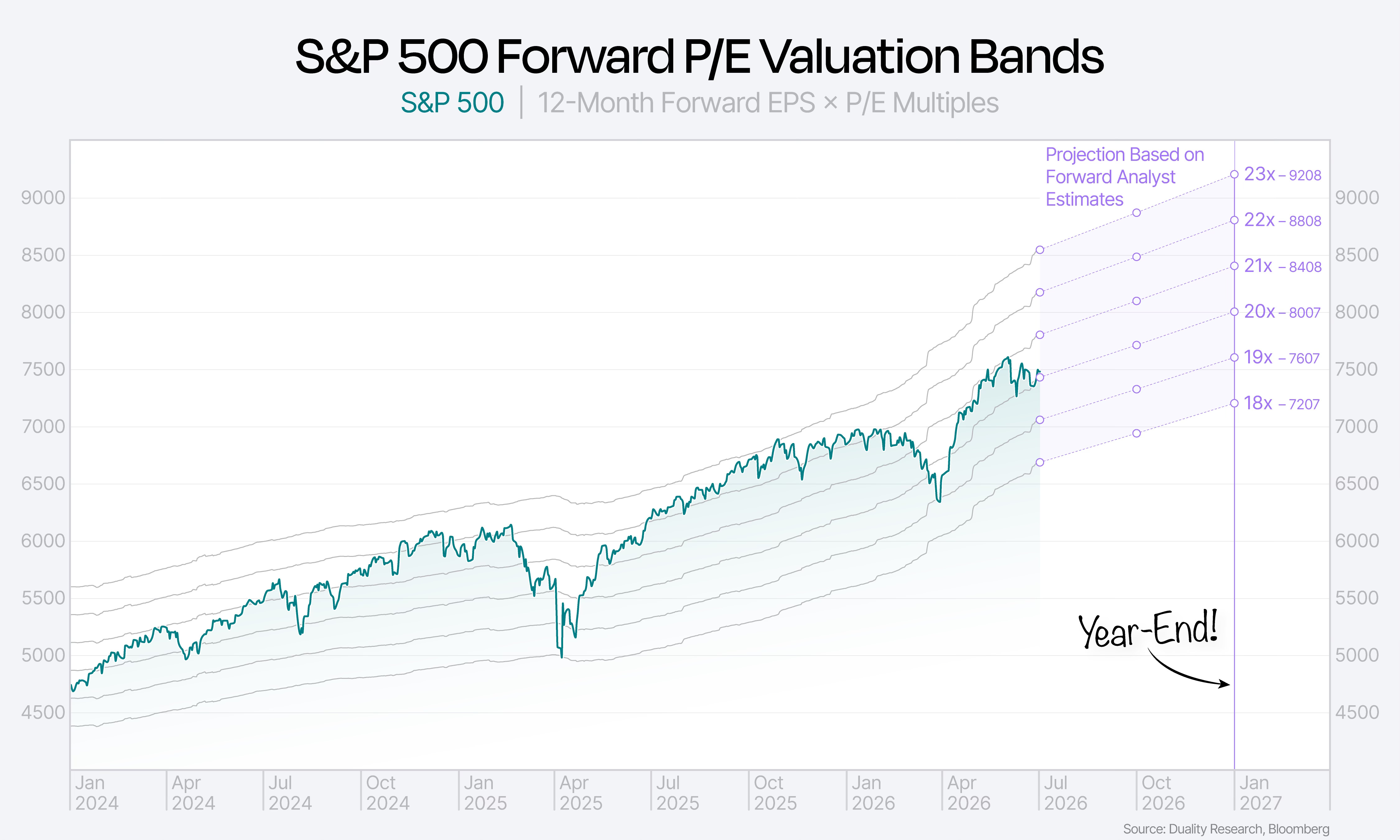

That brings us to our first chart for today. It maps out where the S&P 500 could end up based on current earnings expectations across different valuation multiples.

To put some numbers on it, consensus currently expects 2027 EPS at around $400. If that number doesn’t really change by year-end and valuations stay around where they are today, that gets you comfortably to around 8000 on the S&P 500.

By December 31, 2026, the market will be pricing in 12-month forward EPS, reflecting full-year 2027 earnings.

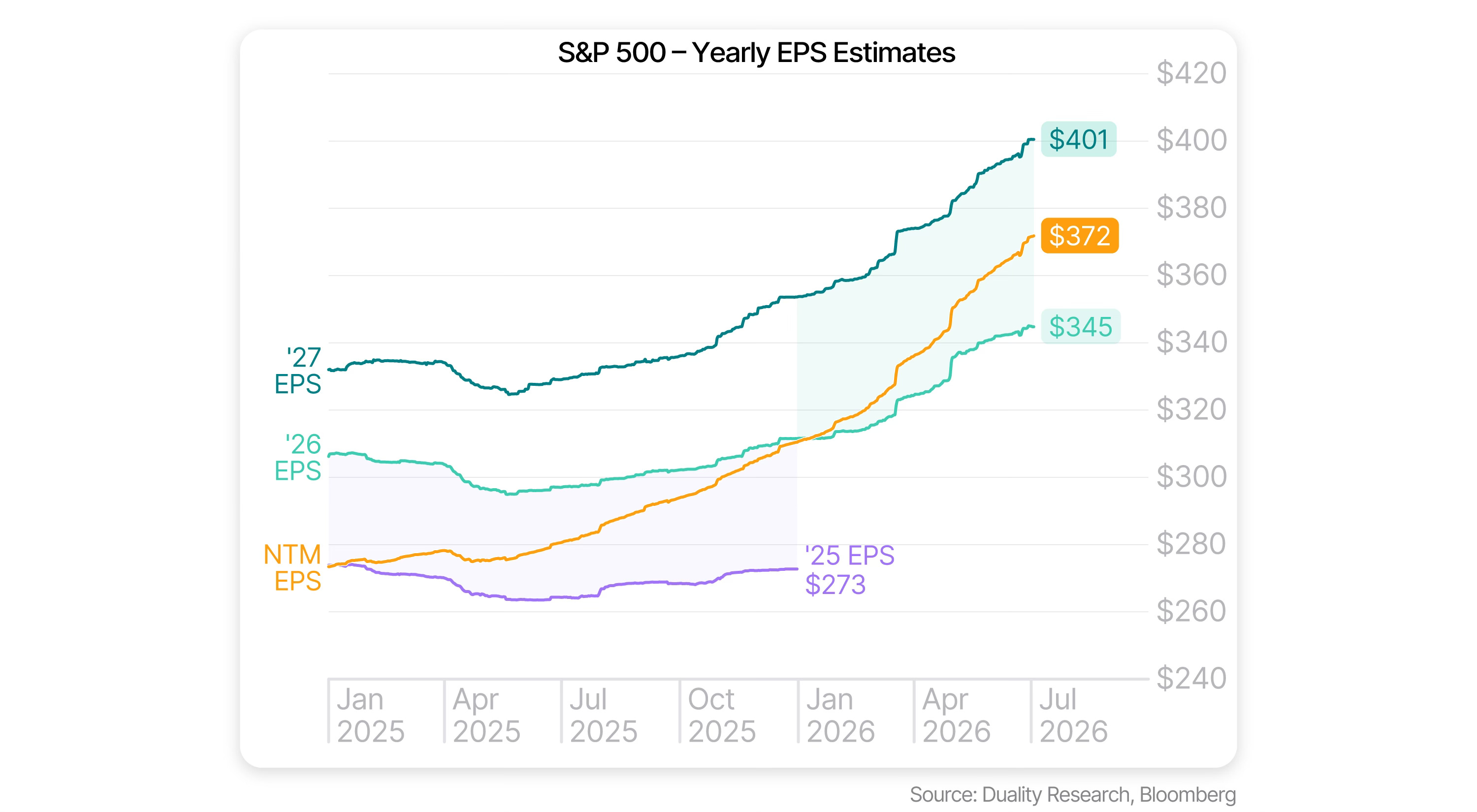

Now, if we look at our next chart, you can clearly see the story in the data: 2027 earnings estimates have been grinding higher pretty much the whole year.

We started 2026 with consensus around $355 for 2027 EPS. Today, we’re already above $400, thanks to the strong earnings momentum we’ve been seeing.

So in that context, assuming $400 by year-end probably isn’t even an aggressive case at this point — if anything, it still looks fairly conservative, unless we get a meaningful macro shock.

So, with $400 maybe still a bit on the low side, we’ve put together a simple valuation and earnings matrix for the S&P 500 so you can mess around with different scenarios yourself. It basically shows where the market could land this year depending on forward P/Es and a range of 2027 EPS assumptions.

For example, if earnings drift another ~5% higher to around $420 by year-end, the S&P 500 still gets to 8000 as long as the forward multiple doesn’t fall below roughly 19x. So, no matter how you slice it, 8000 by year-end still looks like a pretty fair base case for us.

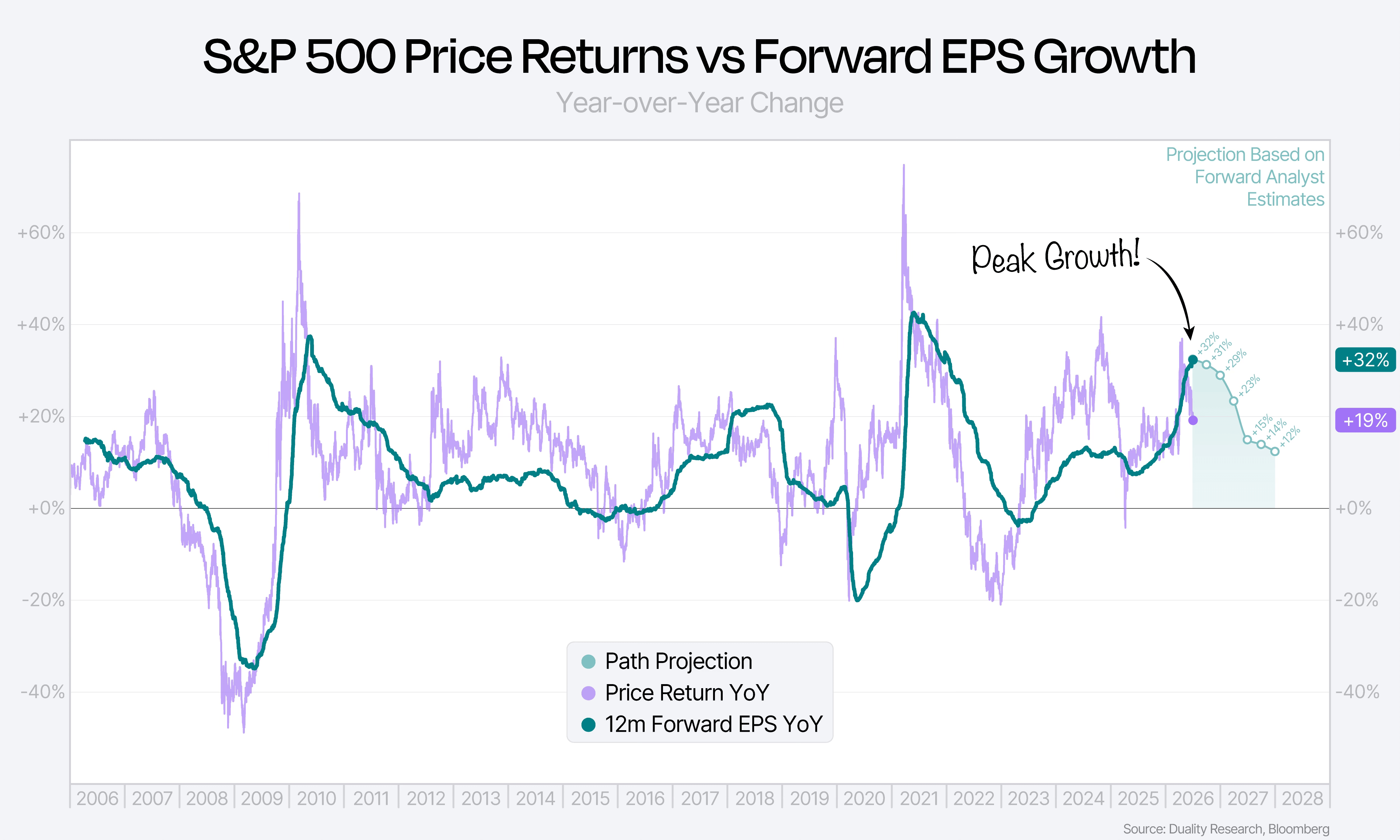

Now, as we mentioned at the start, we’re basically looking at peak growth here. Year-over-year earnings growth has hit a strong 32%, but as our chart below shows, that pace is expected to slow quite a bit over the next 18 months.

We’ve said this before, but it’s worth repeating: once EPS growth rolls over (even if it stays positive), price performance tends to lag earnings growth. And that’s pretty much what we’re already seeing again, with the multiple compression that’s been going on for a while now.

In other words, the big headwind from here — given we’re in a peak growth setup — is that it’s hard to see valuations really expanding much further. If anything, history says this kind of environment usually comes with multiple compression, not expansion. That’s why we think the S&P 500 is probably capped around ~21x forward earnings for the time being.

At the same time though, the market has already done a lot of the work. Over the past few weeks and months, we’ve already seen a solid re-rating, meaning a good chunk of this regime shift is likely already in the price.

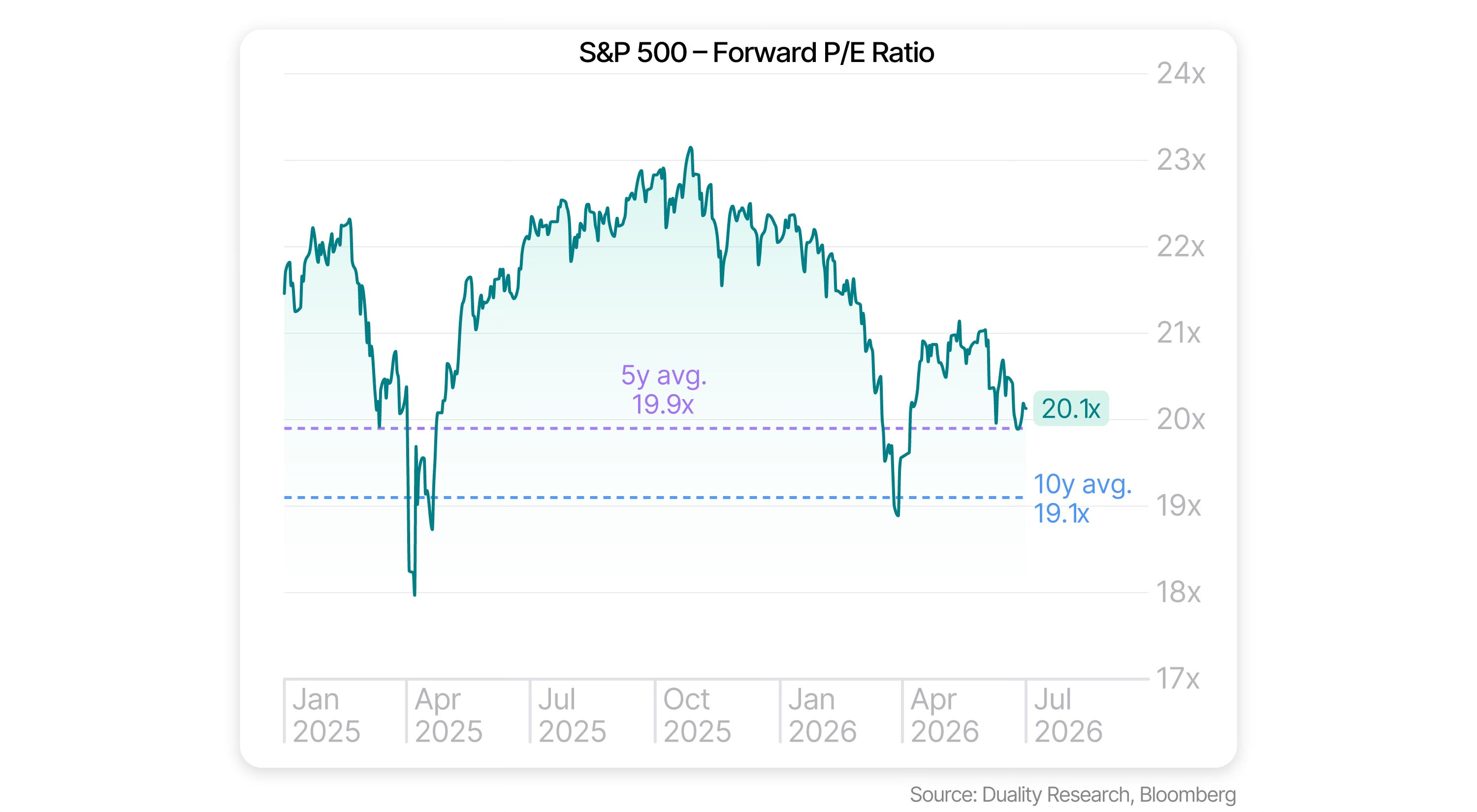

As our chart below shows, valuations aren’t stretched by any means. We’re basically just ~1% above the 5-year average and only ~6% above the 10-year average forward P/E. So it’s hard to call this market expensive — especially when you factor in the much higher profitability we’re seeing today, which in theory typically demands a higher valuation premium, even if that premium is quite obviously non-existent at this point in time.

What this all comes down to is pretty simple: equities still look set to grind higher into year-end, mainly thanks to solid earnings growth projections. At the same time, the market has already done a lot of the work on the other side, re-rating lower to reflect a slower-growth setup.

Putting those two together, it still leaves us with 8000 on the S&P 500 as our base case for year-end, with room for further upside from there — barring any shocks.

This brings us to the second headwind the market is facing as we head into the second half of the year: peak hawkishness. Not only has this been a drag on valuations, but as we’ve said before, the Fed is still the biggest risk to this bull run — since tightening cycles are often what eventually end it.

Right now, this market is still priced for hikes. But we’re willing to fade that view for reasons we’ve laid out before.

Now, whenever you’re willing to fade consensus, the question is always the same: what’s the best trade to express that view. In this case, fading peak hawkishness can work through a couple of channels. Equities — especially the S&P 500 — should benefit if the Fed starts to dial things back. If that comes with a weaker US dollar, Gold is for example another straightforward way to express the same view.

On the equity side, we’re still overweight Tech. While that’s usually a good way to fade peak hawkishness, Tech is starting to show some internal stress, especially with Semis now such a big chunk of the sector. In the meantime, Software stocks and a few of the Mag7 names have actually held up with solid relative strength. So this is starting to look more like something where we need to be a bit more selective, rather than just owning the whole sector that’s nearly 50% Semis. That said, as long as Tech’s relative strength holds above last year’s high, we’re sticking with the overweight — for now.

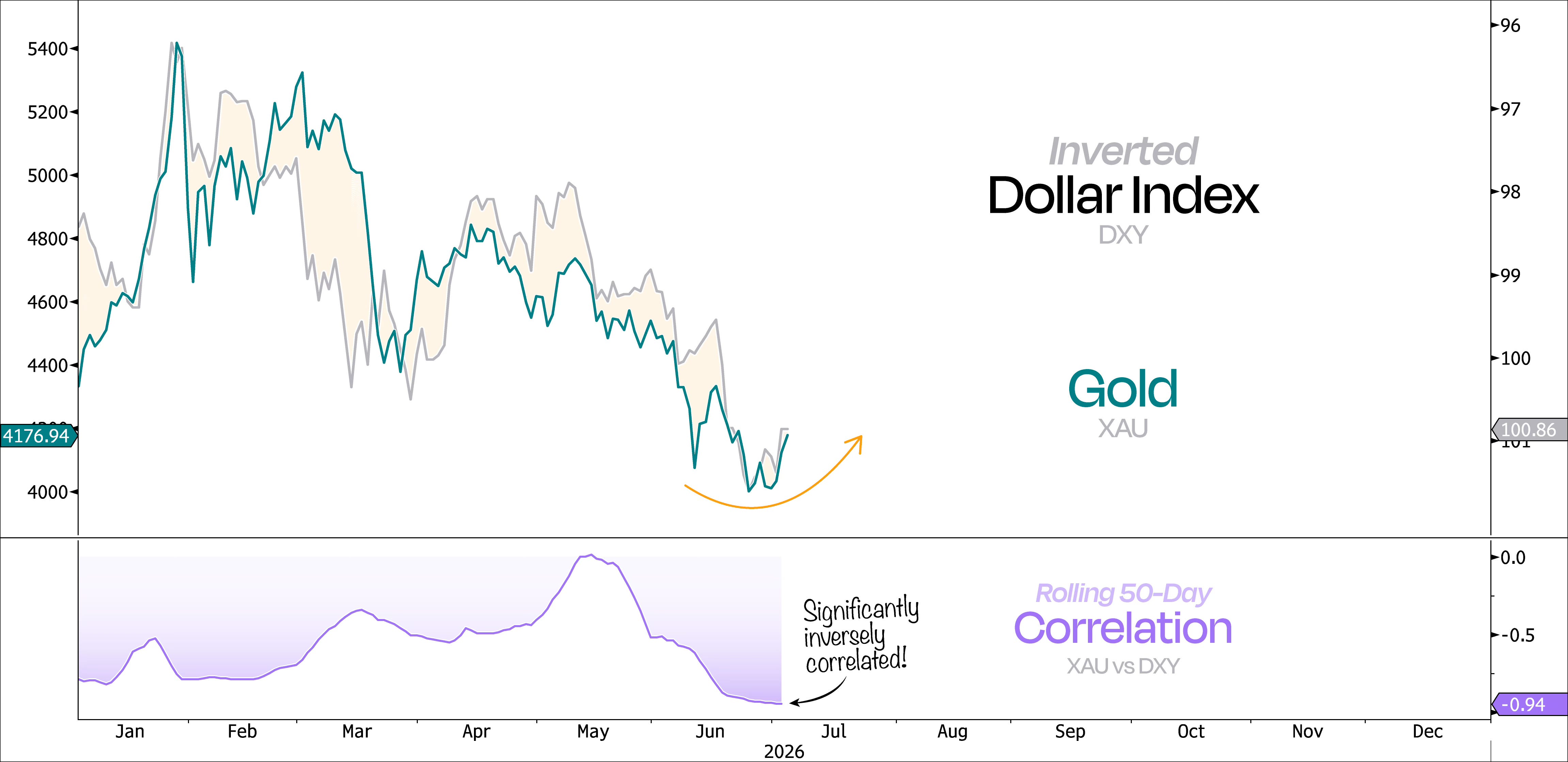

For a cleaner, less equity-correlated way to fade peak hawkishness, we’re adding Gold here via GLD. As we mentioned before, the US dollar is still bid, especially after Warsh didn’t explicitly push back against the market’s hawkish repricing. And as our next chart shows, the Dollar Index and Gold are basically perfectly inversely correlated right now, with a rolling 50-day reading at -0.94 — an extremely strong inverse relationship. So if the dollar rolls over, Gold should be quick to catch a bid.

What’s also nice here is that Gold gives us a pretty clean risk level to work with. A weekly break below $360 would likely open the door for more downside. That said, as our next chart shows, Gold has already tested that level while traversing peak hawkishness in recent weeks.

If the Fed starts to soften from here, Gold should stay supported — mainly through a likely reversal in the dollar. For us, this is really just a tactical way to fade peak hawkishness, with a target range of $400–$420 over the summer — basically back to where Gold was trading before the hawkish repricing.

On the downside, a clean break of $360 takes us out. That keeps the risk on the trade at roughly ~5% of deployed capital.

So, where does that leave us?

Fading peak geopolitical uncertainty and peak inflation fears in the first half of 2026 ended up being a strong driver of performance for us. Now, heading into the second half of the year, the backdrop has shifted to peak growth and peak hawkishness.

Peak growth is more of a condition than a trade, but as we’ve already laid out, the market has largely re-rated to reflect it, especially with earnings growth set to slow meaningfully from here.

Peak hawkishness, on the other hand, is a much clearer consensus call — and one we’re actively fading. We’re doing that through continued exposure to risk assets, while also adding Gold, which should benefit if the US dollar starts to give back some of its recent strength that’s been weighing on precious metals.

If we’re right and the Fed starts shifting toward a more dovish stance over the coming weeks and months, we think the biggest tail risk for this bull market stays contained. In that scenario, this earnings-driven market should be able to comfortably lift the S&P 500 to at least 8000 by year-end, with room to push closer to 8500 if we simply hold today’s valuations and see 2027 EPS drift toward ~$420 by December.

And yes — just like we said six months ago, the “bubble” talk will likely only get louder as this bull market grinds higher. But in our view, this market is still fairly valued — not just today, but even looking out six months from now, potentially with another ~13% upside from here.

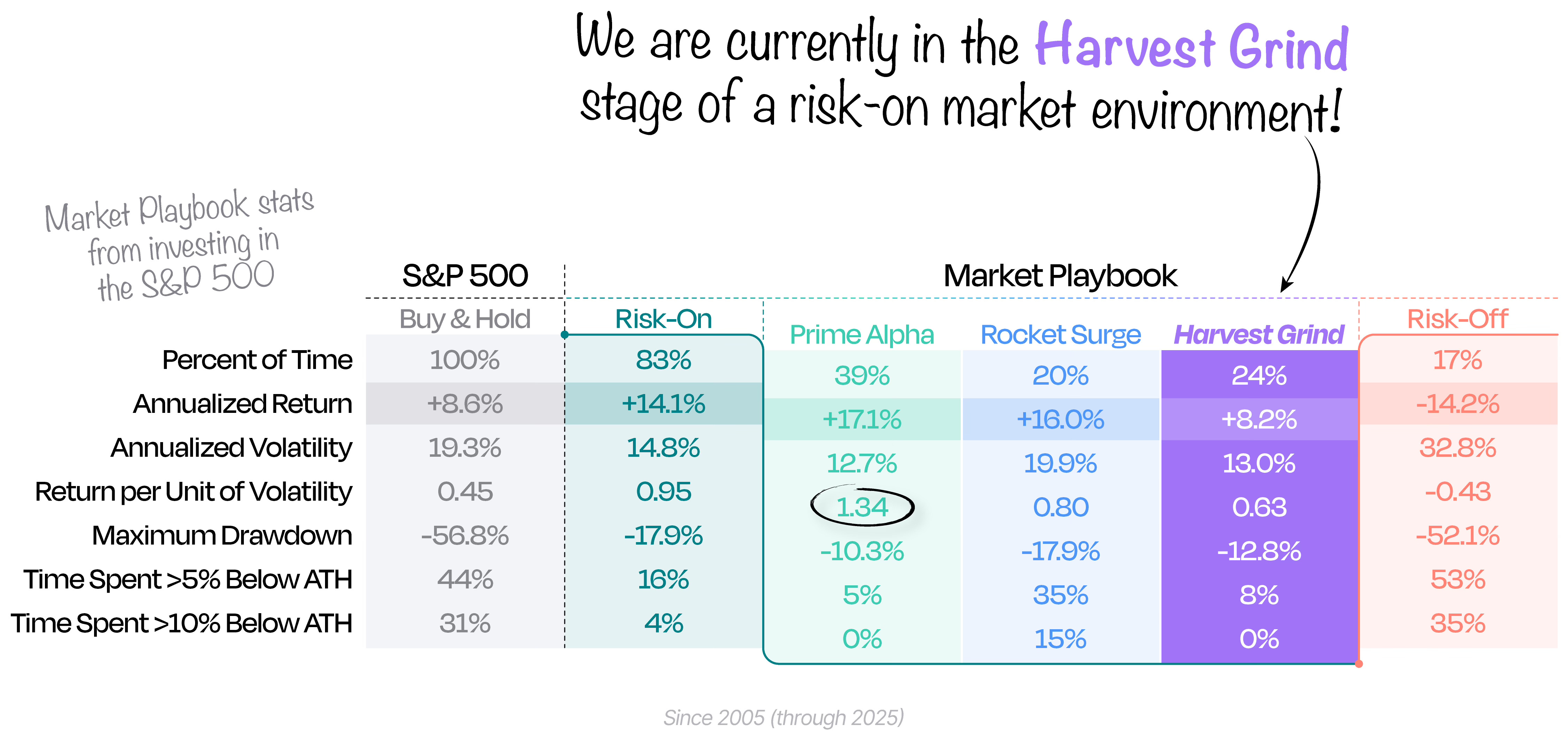

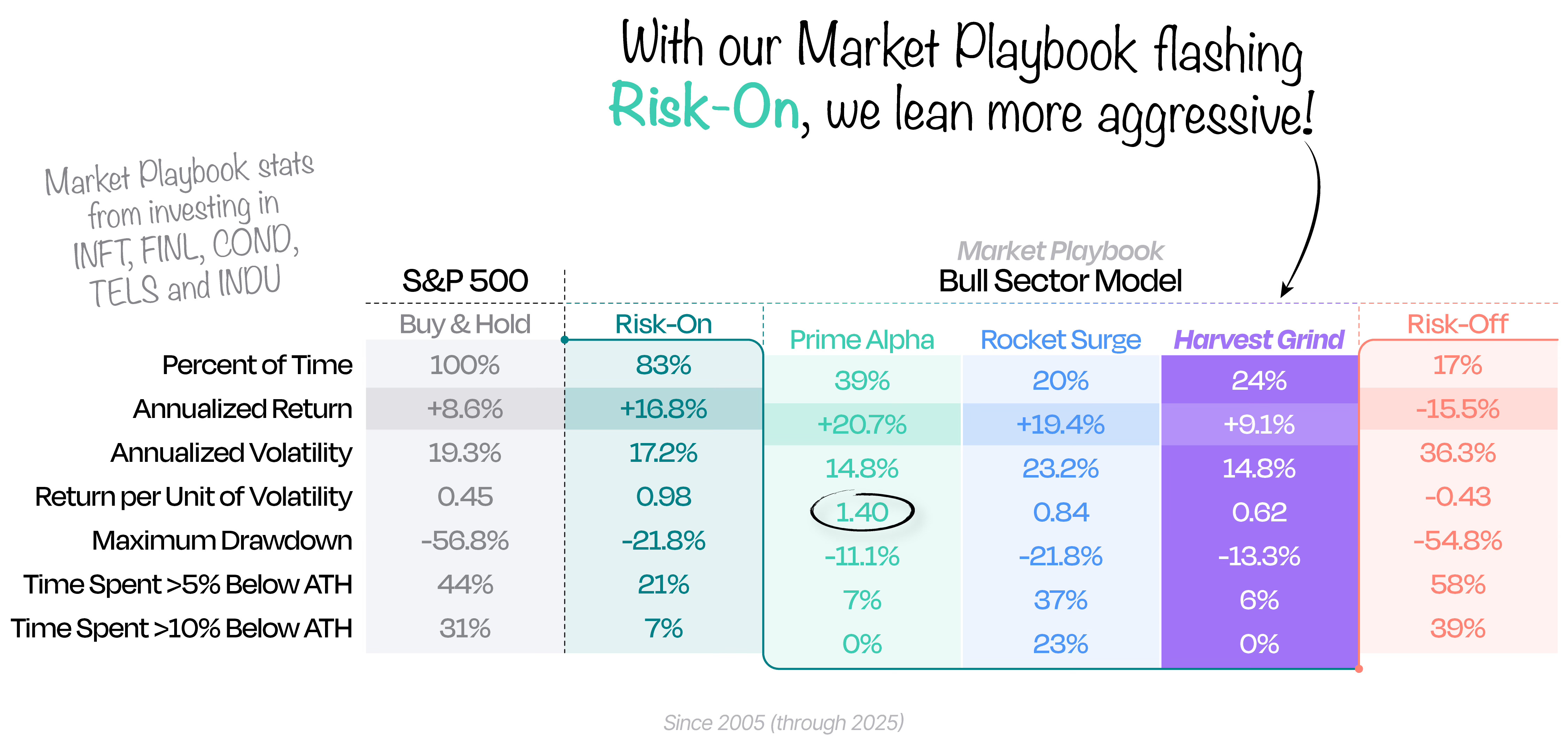

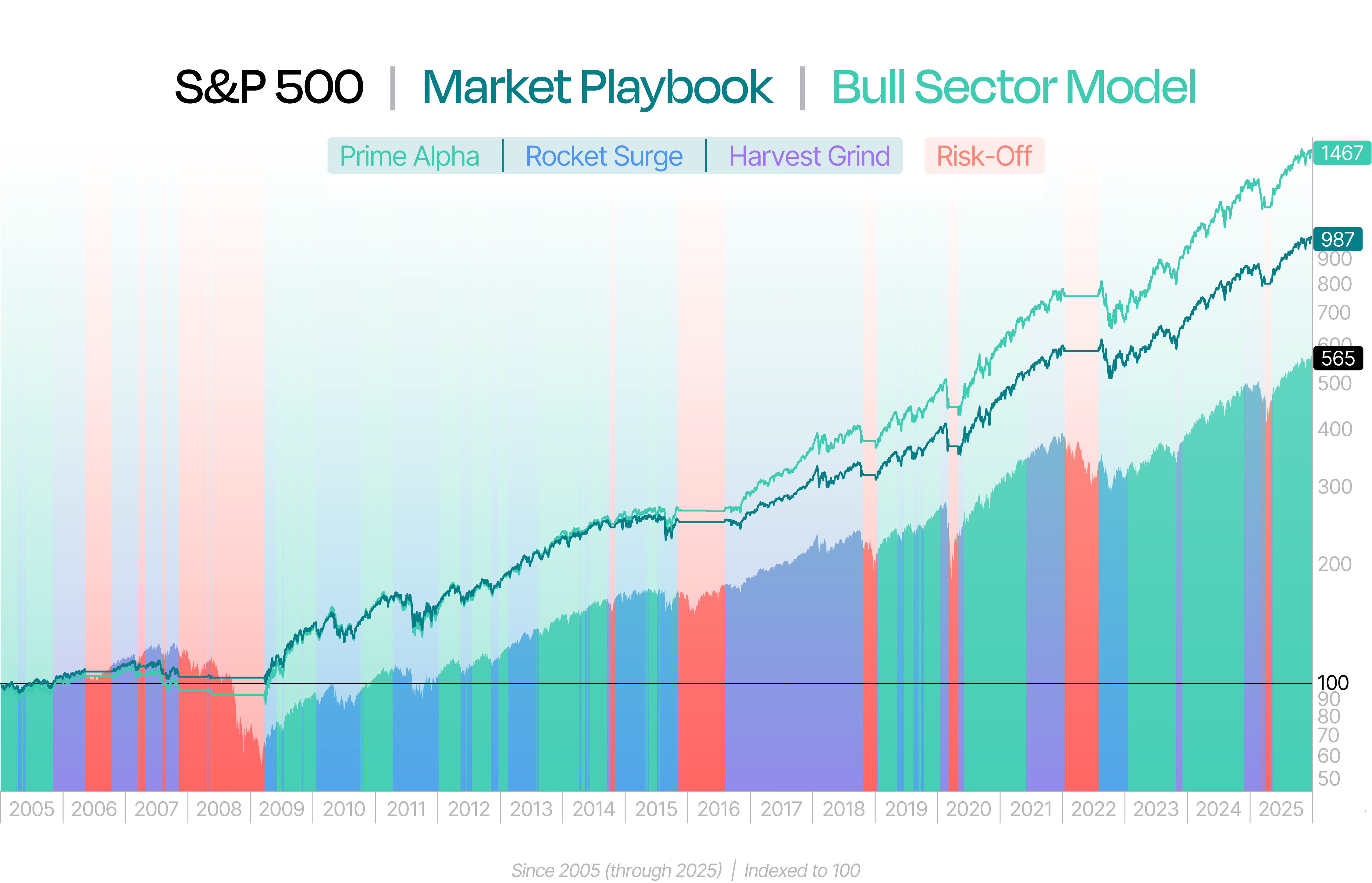

♟️ Duality Research — Market Playbook Status ♟️

{kind=link}

Keep reading with a 7-day free trial

Subscribe to Duality Research to keep reading this post and get 7 days of free access to the full post archives.