Tiny Selloff, Major Valuation Reset

Thoughts on the Market

As we write today, there’s unfortunately not much positive to report from last week.

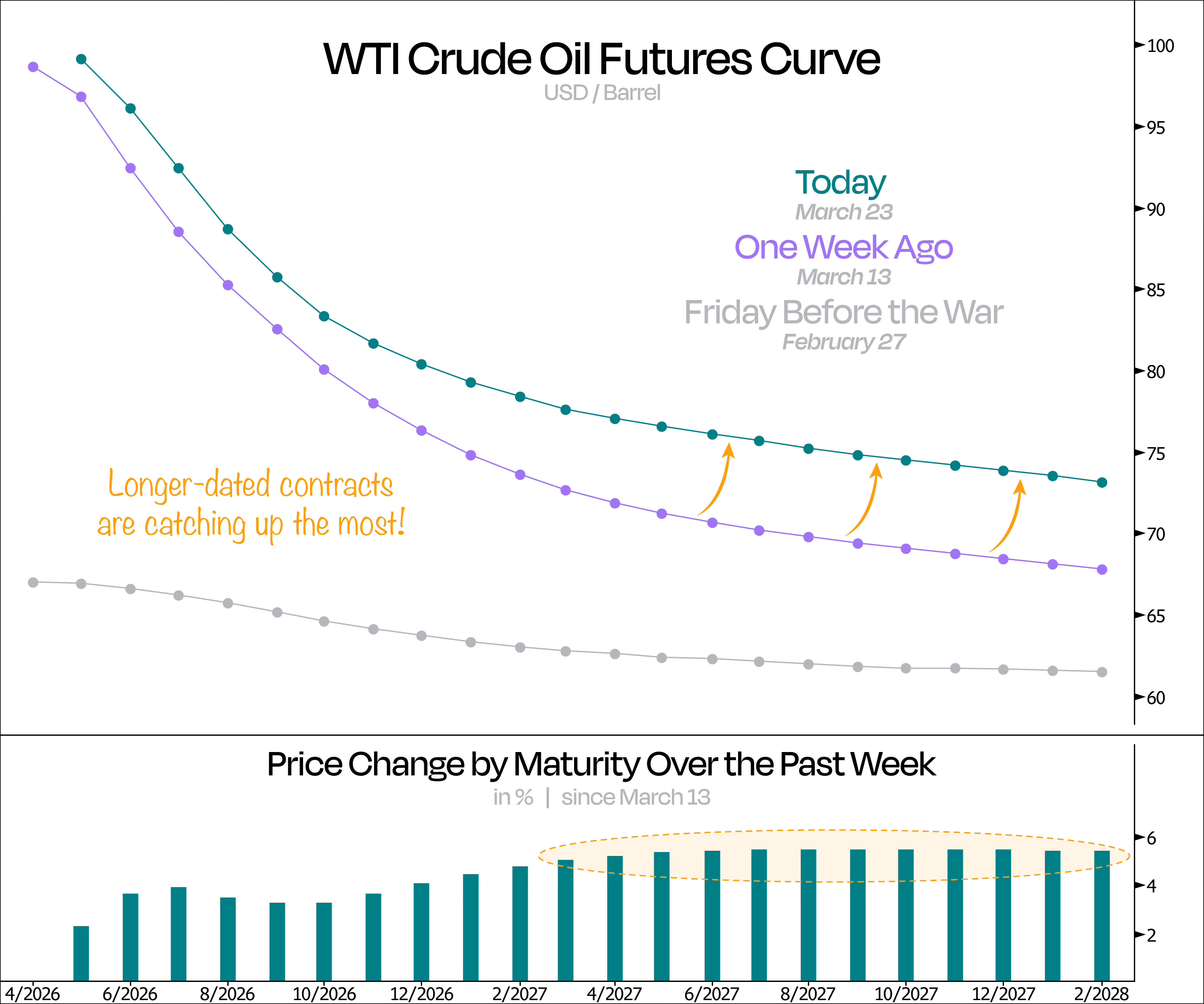

A quick look at our first chart shows that markets are increasingly treating this oil supply shock as something that’s here to stick around. This is especially clear when we look at how prices moved along the oil futures curve last week: even though front-month prices dipped slightly, longer-dated contracts moved notably higher.

While the curve isn’t necessarily predictive of future prices, it does reflect current supply–demand dynamics. And right now, it continues to flatten at much higher levels — basically suggesting the market isn’t expecting much relief anytime soon.

Like we’ve been saying, this is inevitably going to choke the global economy — with time being the critical factor here.

In the coming weeks, people will dip into their savings just to keep living their usual lives, but eventually they’ll have to cut back once literally every consumer item gets repriced. And with oil around $100, it’s not a question of if, just when.

Now, as if that wasn’t enough pressure, we now have central bankers turning hawkish into a supply shock.

Raising rates because a strait is closed? That’s like a doctor prescribing you beta-blockers to slow your heart rate while ignoring a massive clot in your aorta. It’s the wrong tool for the problem — but that’s exactly what’s happening here, with policymakers trying to fix a supply issue using demand-side tools.

It feels like they’re stuck in textbooks instead of dealing with reality. And if anything, the hit to growth from lower real incomes argues for easing, not tightening, to keep demand from rolling over.

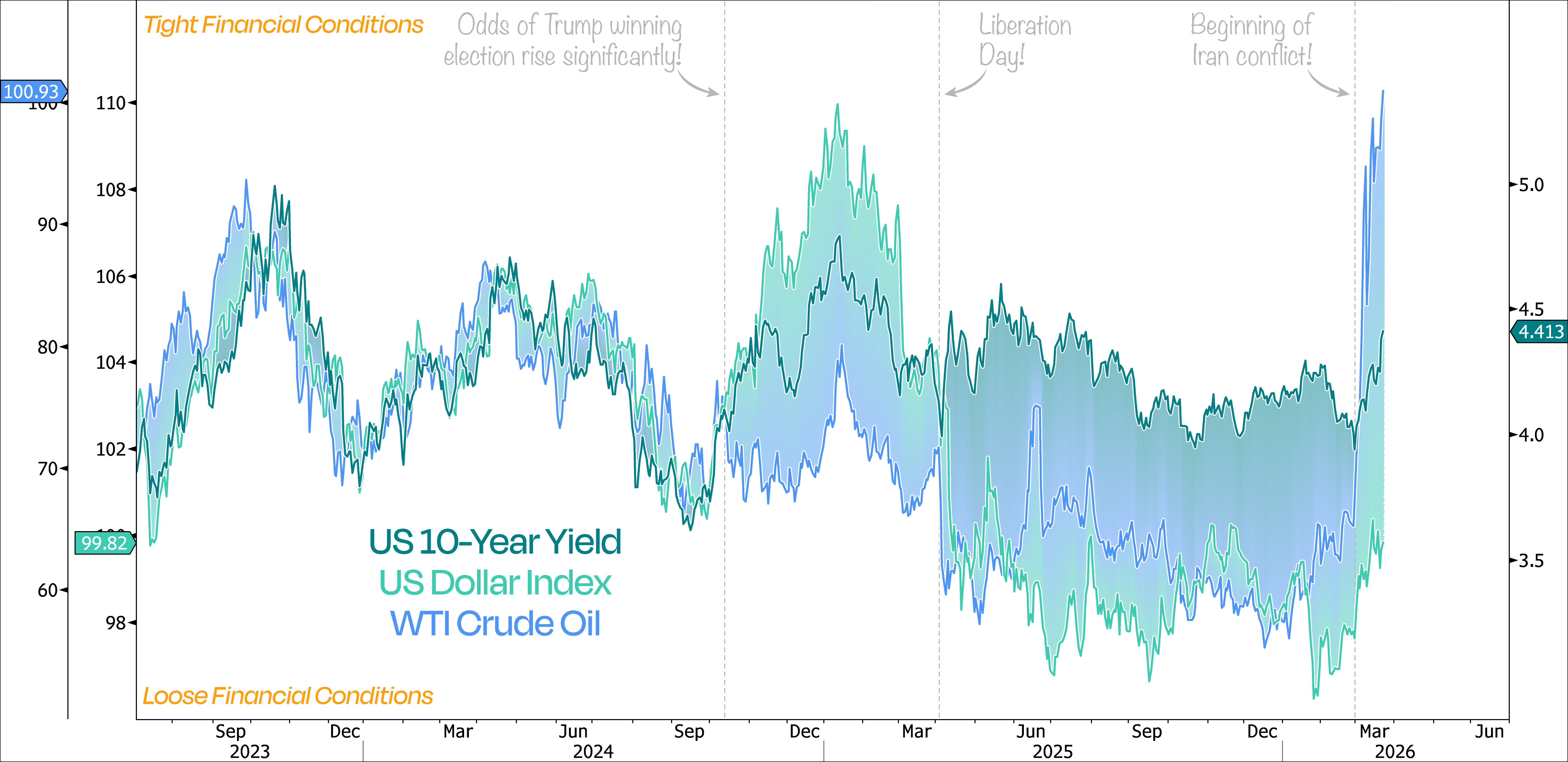

At the end of the day, though, it’s not about what we think they should do — it’s about what they actually do. And right now, all this hawkish talk is triggering a sharp repricing that’s adding even more pressure on the global economy and risk assets, with financial conditions already getting pretty tight.

Financial conditions are essentially a function of interest rates, oil prices, and the US dollar.

As a result, the backdrop for equities keeps getting worse, and we just got stopped out of our small-cap trade last week — which isn’t too surprising given it’s the most sensitive to tighter financial conditions and slowing growth.

At its core, that trade is basically a short on Tech and, to some extent, Growth. But when growth opportunities become scarce, that’s exactly when Growth stocks tend to outperform.

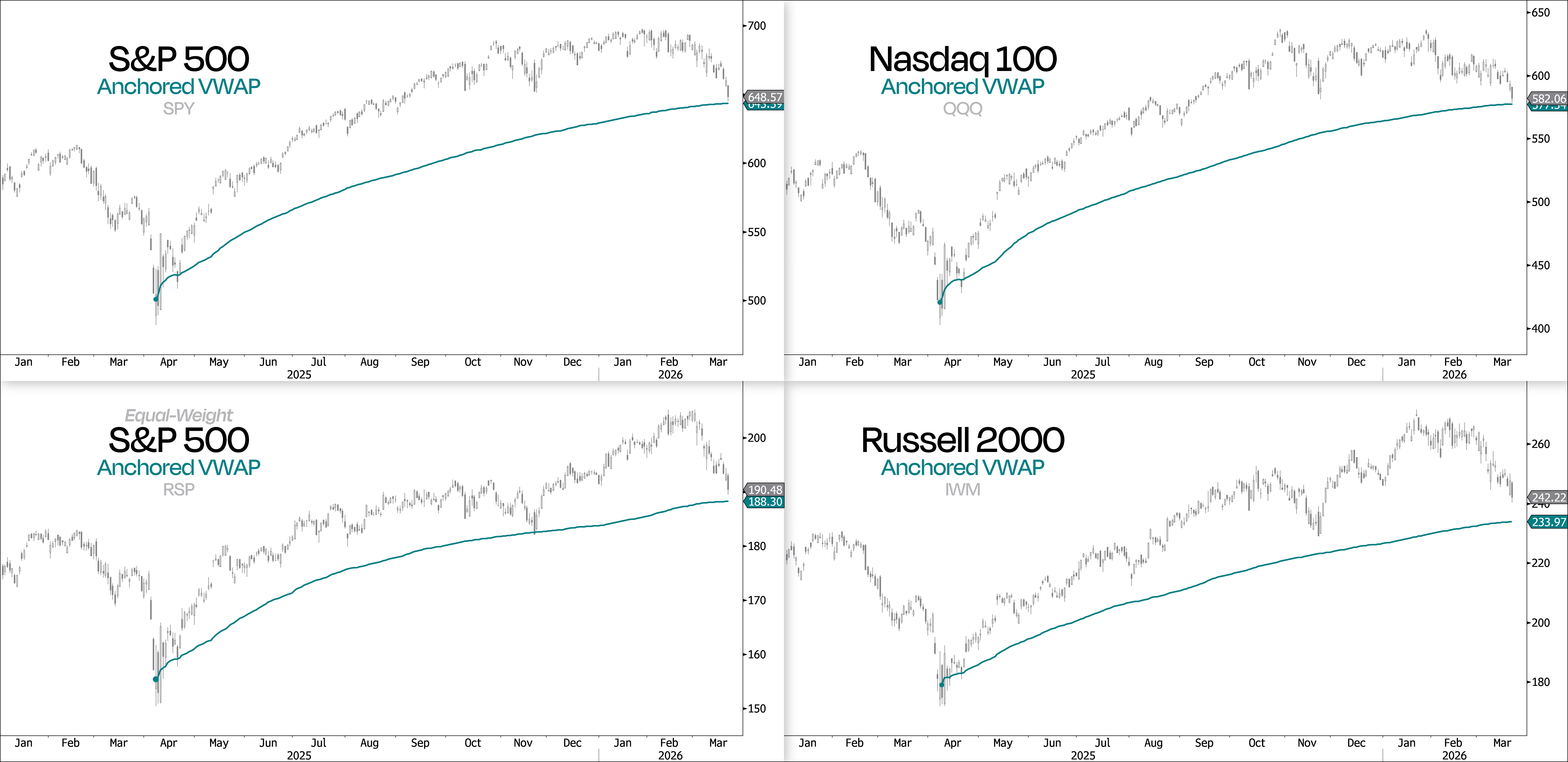

That said, we’re still invested in the S&P 500, which naturally leans toward Growth given its cap-weighted structure. As discussed two weeks ago, we don’t think that another 1-3% decline in the S&P 500 is too heavy a price to pay for continued exposure to US equities over the longer term — especially with how oversold things have gotten. Friday’s options expiry likely added to that, with some forced selling exaggerating the move.

Why 1%? That’s where the anchored VWAP from last April’s low sits. Stretch it to 3%, and you’re basically in correction territory (around -10% from the highs), which is something we usually see about once a year anyway.

So while last week’s focus was on whether the 200-day moving average will hold, we think there’s likely more buying interest in the -1% to -3% range — roughly 6280 to 6440 on the S&P 500.

And interestingly, the Nasdaq 100, the equal-weight S&P 500, and the Russell 2000 are all showing a similar setup when you look at their anchored VWAPs from last year’s tariff selloff lows.

What’s interesting is what this long consolidation — now followed by this selloff — has actually done to valuations.

Keep reading with a 7-day free trial

Subscribe to Duality Research to keep reading this post and get 7 days of free access to the full post archives.